Stablecoin Integration: The Definitive Link Toward Everyday Payments

Global financial infrastructure is undergoing a structural transition where digital custody connects directly with the real economy. The issuer Circle reported more than 20 trillion settled in USDC by January 2025. This evolution redefines programmable money, reducing friction between storing crypto assets and spending them commercially.

The dominant narrative assumes that cryptocurrencies operate exclusively as high-risk investment tools. However, the penetration of corporate payment networks debunks this perception. Understanding this shift becomes imperative when analyzing the systemic interoperability of current markets.

The convergence between traditional systems and digital assets accelerates institutional adoption. Multinational corporations already process significant volumes using decentralized rails, an obvious leap since Visa launches pilot for stablecoin payments funded with fiat for US businesses, optimizing treasuries and consolidating enterprise utility.

This corporate strategy is backed by strictly measurable adoption metrics. The payment network itself reported sustained quarterly growth in April 2026, reaching an annualized rate of 7 billion in stablecoin settlement volume. The figures confirm the transition toward standardized commercial settlement.

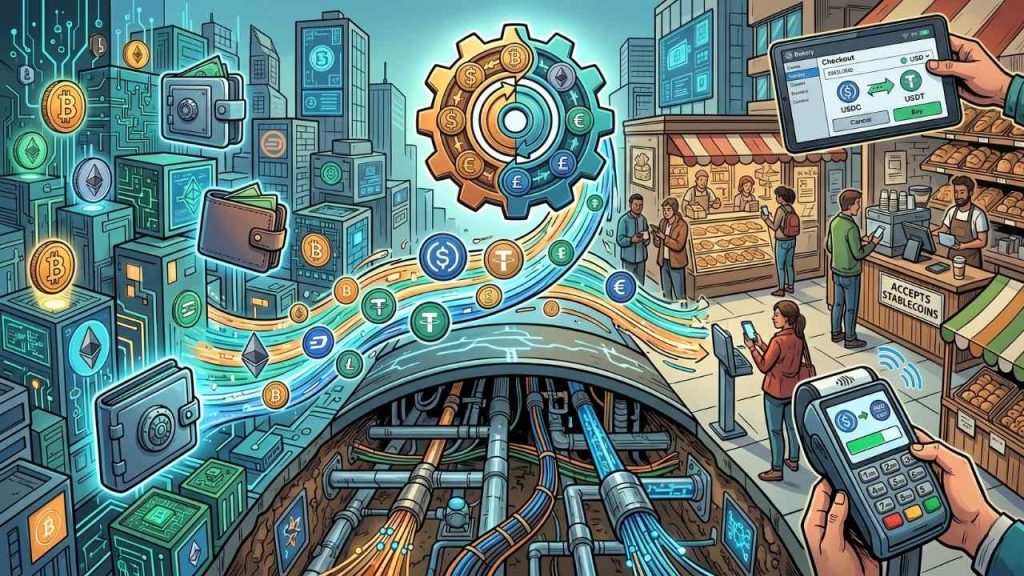

At the commercial infrastructure level, processing platforms are rapidly modifying their terminals to accept decentralized flows. The largest e-commerce processors in the global market have once again enabled institutional support for these exact transactions.

This reinstatement allows international merchants to collect directly via blockchain networks. Stripe’s official documentation establishes limits of 10,000 dollars per processed transaction, settling the final balance in traditional fiat currency. The corporate bridge is functional.

Comparative evolution of infrastructure

The comparative historical context offers a perfectly clear perspective on this financial adoption phenomenon. During the 1950s, the initial introduction of credit cards faced severe resistance due to the extreme fragmentation of commercial point-of-sale terminals.

Early bank plastics required entirely manual telephone verifications and extensive weekly printed lists just to actively mitigate commercial fraud risks. The global standardization of magnetic stripes finally allowed the implementation of true instantaneous electronic settlement. Standardization reduces operational execution friction.

Current stablecoins are undergoing exactly that same phase of structural technological standardization. Non-custodial wallets act as the new physical payment terminals, while layer-two protocols function precisely as the modern magnetic authorization networks, lowering transactional costs.

The opposing view argues that complex user experience will permanently block retail adoption. Skeptics maintain that managing private keys and tolerating structural network volatility will continuously deter the average everyday consumer from participating.

This position is completely valid if one analyzes the technological state of the year 2021. The complexity of graphical interfaces and high network commissions during congestion periods excluded daily micro-payments, limiting usage to large-volume institutional transfers.

However, the skeptical thesis is invalidated by the aggressive advancement of user-centric design. Account abstraction allows recovering wallets without complex seed phrases, while sponsored payments hide network gas fees strictly behind instant commercial corporate transactions.

Autonomous agents optimize real-time capital flows, a milestone that makes sense given that Coinbase’s agentic wallets pose a structural risk due to financial autonomy, rapidly expanding the established transactional boundaries across the digital ecosystem.

European regulatory certainty provides a remarkably solid foundation for this rapid commercial expansion. According to a University of Vienna report published in December 2024, Circle is the only authorized issuer under MiCAR, guaranteeing strict compliance. Regulations provide clear operational clarity.

The existence of formal licenses for decentralized electronic money issuers effectively mitigates counterparty risks. Commercial banks can now interact directly with these digital reserves knowing there is ongoing prudential oversight and strict immediate liquid capital requirements.

Implications for the transactional economy

The implications of this technological convergence radically alter the structure of international operational costs. The traditional correspondent banking model imposes settlement fees that still average roughly six percent of the total transferred monetary value. Traditional intermediaries lose absolute relevance.

In direct contrast, settlements operating over intermediate layer networks execute cross-border transfers for mere fractions of a cent. Today, global logistics providers and independent freelance platforms formally demand these innovative payment channels to successfully maximize their operational profitability.

The ecosystem is gradually advancing from a logic fundamentally centered on speculative storage toward a high-speed infrastructure. Balances no longer remain entirely idle awaiting appreciation, but actively rotate in the real economy to acquire tangible goods.

This rapid rotation of digital capital requires strictly fluid entry and exit channels. Financial consortiums have understood that capturing continuous conversion commissions is much more profitable than attempting to prohibit the monetary flow toward these distributed ledger architectures.

Shrinking the functional distance between digital wallets and commercial terminals forcefully democratizes access to global commerce. A user in an emerging market can access the same exact level of transactional efficiency as a multinational corporation in a developed financial hub.

The integration of stablecoins within retail commerce completely eliminates international exchange friction. A consumer can stably hold their capital in dollarized digital assets and execute purchases in physical stores that operate exclusively with euros or yen.

The conversion mechanism securely occurs in the background through institutional liquidity providers. The end user experiences instant settlement identical to a traditional debit card, while the merchant formally receives their local currency without any exposure to cryptographic asset volatility.

This architectural design effectively solves the widespread historical problem of global liquidity fragmentation. Global payment platforms actively aggregate corporate demand and strategically route daily transactions through the most structurally efficient blockchains in terms of both temporal and financial performance.

The transition toward this daily use-oriented financial infrastructure definitively discards the previous narrow niche approach. Digital wallets actively abandon their passive role of basic key storage to become highly comprehensive financial interfaces with immediate global commercial settlement capacity.

If stablecoin settlement volume on corporate networks maintains quarterly growth consistently above thirty percent, the vast majority of traditional legacy payment processors will inevitably integrate native on-chain automated settlements well before the end of fiscal year 2028.

This article is for informational purposes only and does not constitute financial advice.