Aave vs MakerDAO: Capital Efficiency vs Monetary Stability in DeFi Lending

The architecture of decentralized finance has ceased to be a monolithic block, splitting into two divergent operational philosophies. Aave and MakerDAO represent the culmination of these paths, where one prioritizes capital velocity and the other the integrity of its own monetary unit.

This distinction is essential for understanding why both protocols dominate the lending sector without completely cannibalizing each other. While Aave acts as a multi-asset liquidity facilitator, MakerDAO functions as a credit issuer under a model similar to a digital central bank.

Liquidity Structures and Risk Management

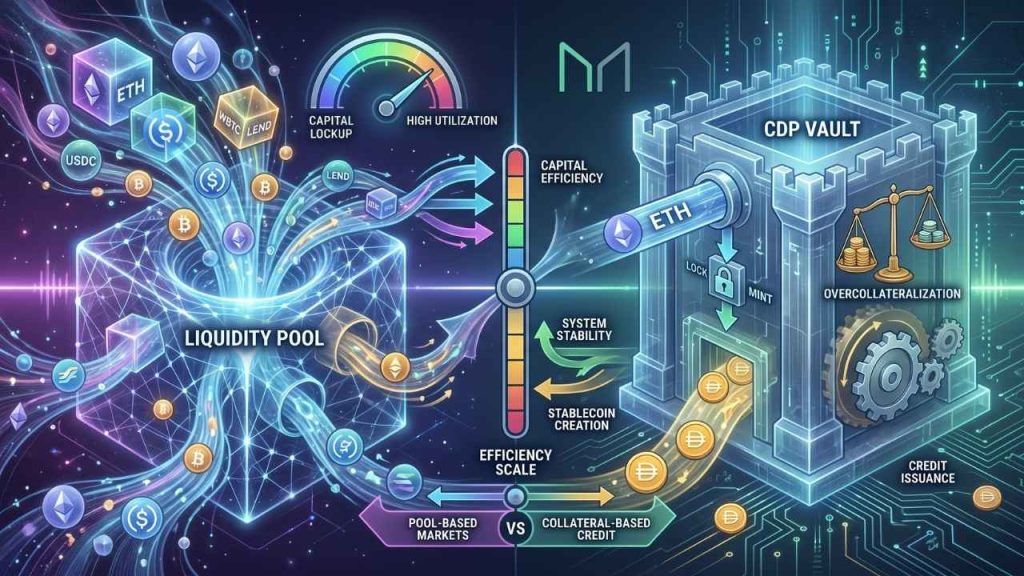

Aave has consolidated itself as a money market based on the peer-to-pool model, where supply and demand dictate rates. As detailed in the Aave V3 Technical Paper, its primary focus lies in optimizing the efficiency of deposited assets through high-efficiency modes (E-Mode).

This system allows users to maximize their borrowing capacity when using correlated assets. However, the protocol’s agility introduces complex variables, as systemic risk in Aave depends on how algorithmic liquidity responds to extreme volatility events in highly interconnected markets.

For its part, MakerDAO, now under the Sky brand, operates through Collateralized Debt Positions (CDP). The user does not borrow the asset from another provider but mints DAI or USDS against their collateral. This allows for superior resilience during extreme volatility in terms of interest rate stability.

The MakerDAO protocol has evolved to include Real World Assets (RWA), seeking to diversify the backing of its stablecoin. Nevertheless, this opening has generated internal governance friction, especially when in 2012 surged arose about MakerDAO community concerns over the new control of WBTC and its impact on collateral security arise.

The most notable technical difference lies in interest rate management. In Aave, rates are dynamic and adjusted through programmed utilization curves. This ensures there are always incentives for liquidity providers to maintain the capital flow necessary for market operation.

In contrast, MakerDAO uses governance parameters to set stability rates. As noted in the BIS Working Paper No 1061, protocols that issue their own currency face unique challenges in managing solvency compared to pure lending markets.

The MakerDAO model is vertical, controlling everything from issuance to asset burning. Aave is horizontal, connecting various markets and chains. This horizontal structure allows Aave to be more versatile, but it also exposes it to security failures in any asset acting as collateral.

To mitigate this, Aave introduced isolation silos and supply limits in its V3 version. Details on these security measures can be found in the official Aave V3.3.0 Audit Report, which analyzes defenses against oracle manipulation attacks.

Flexibility vs. Monetary Sovereignty

From a critical perspective, the Aave model could be considered more vulnerable to cascading liquidity crises due to its interdependence. If a collateral asset loses its parity or liquidity, the speed at which the protocol must liquidate positions tests the underlying network infrastructure.

In contrast, MakerDAO proponents argue that issuing its own stablecoin provides the monetary sovereignty necessary for long-term stability. However, this view is valid only if the protocol can maintain DAI’s parity without sacrificing decentralization—a difficult balance to sustain.

Monetary sovereignty in open networks is MakerDAO’s goal, but the increasing reliance on centralized collateral like USDC questions this premise. If regulators act on the underlying assets, MakerDAO’s supposed resistance could be more deeply compromised than Aave’s.

The thesis that Aave is superior for its capital efficiency would be invalidated if a failure in algorithmic liquidity logic caused massive bad debt. On the other hand, the MakerDAO thesis would fall if the centralization of its reserves eliminated its value proposition as a banking alternative.

Both protocols face the challenge of governance under constant regulatory pressure, forcing technical decisions that often sacrifice simplicity. The migration toward more complex models aims precisely to absorb financial shocks that in the past proved fatal for smaller protocols.

The integration of the Sky Ecosystem represents MakerDAO’s attempt to scale its institutional reach. This strategy seeks to reduce protocol revenue volatility, although it introduces new risk vectors related to traditional asset custody and international regulatory compliance.

Efficiency in collateral management will be the definitive battleground between these two giants. Aave bets on automation and risk fragmentation by markets, while MakerDAO leans toward more active treasury management centralized in its risk committees.

If the volume of real-world assets in MakerDAO exceeds 60% of its backing, the protocol will behave more like a traditional bank than DeFi infrastructure. This transition will radically alter the perception of risk for users seeking refuge in pure decentralization.

In Aave’s case, its success will depend on the ability to maintain liquid markets in Layer 2 networks. The dispersion of liquidity across multiple chains is a technical challenge that could erode the capital efficiency that makes it so attractive to users today.

If liquidity remains fragmented and liquidation costs increase in secondary networks, Aave could face local solvency issues. Data shows that the resilience of these systems is not static but evolves with the behavior of market agents.

This article is for informational purposes and does not constitute financial advice.